Fusion Micro Finance, located in New Delhi and established in 2010, is a micro-lending company that provides funding to women in rural and semi-urban regions so they may take advantage of more options for employment. Fusion offers loans up to Rs. 50,000 and employs a joint liability group concept created by the Grameen Bank of Bangladesh.

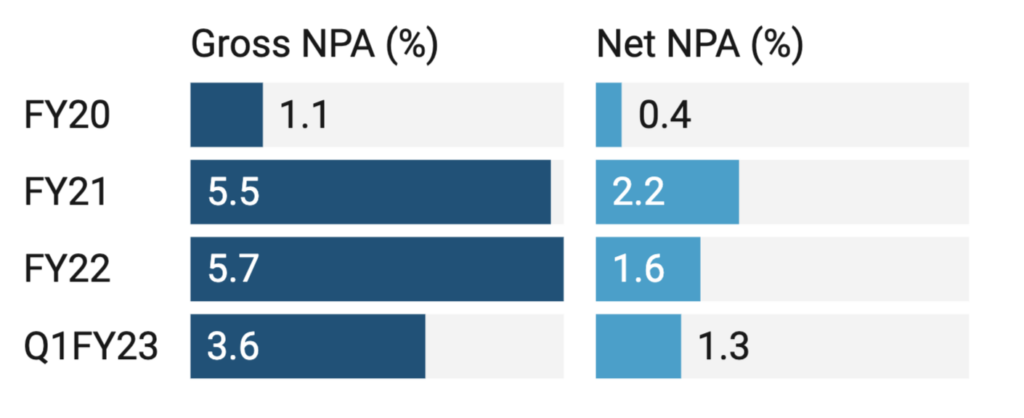

As of June 30, 2022, and March 31, 2022, 2021 and 2020, total AUM stood at ₹7,389.0 Cr, ₹6,785.9 Cr, ₹4,637.8 Cr and ₹3,606.5 Cr respectively. As of June 30, 2022, the share of AUM from customers in rural areas represented 91.3% of the total AUM. FMFL’s focus customer segment is women in rural areas with an annual household income of up to ₹300,000. Their business runs on a joint liability group lending model wherein a small number of women form a group (typically comprising five to seven members) and guarantee one another’s loans. As of June 30, 2022, and March 31, 2022, 2021 and 2020, gross NPA ratio was at 3.6%, 5.7%, 5.5% and 1.1%, respectively, and net NPA ratio was 1.3%, 1.6%, 2.2% and 0.4% respectively.

IPO Details

IPO Date

Nov 2, 2022 to Nov 4, 2022

Listing Date

11 November 2022

Price Band

₹350 to ₹368 per share

Lot Size

40 Shares

Issue Size

₹1,104 Cr ( ₹600 Cr Fresh, 504 Cr Offer for Sale)

Minimum Application

₹14,720

GMP (Last Updated 31st Oct)

₹33 per share

QIB Quota

50% of the Issue Size

NII Quota

15% of the Issue Size

Retail Quota

35% of the Issue Size

Schedule

Issue Period

Nov 2, 2022 to Nov 4, 2022

Finalization of Allotment

10th November 2022

Initiation of Refunds

11th November 2022

Credit of Shares

14th November 2022

Date of Listing

15th November 2022

Anchor Investors Lock-In End Date

4th December 2022

Objects of the Issue

Augment the capital base of the microfinance firm.

Financial Highlights

Date

Q1 FY23

FY22

FY21

FY20

Revenue (₹ Crores)

342.72

1151.26

855.81

720.26

Net Profit (₹ Crores)

75.1

21.75

43.94

69.61

EPS (diluted)

8.98

2.64

5.49

10.32

Asset Quality

Strengths

Diversified and extensive pan-India presence: As of June 30, 2022, the company had 29 lakh active borrowers who were served by 966 branches and 9,262 employees across 377 districts in 19 states and UTs in India. No single state contributed to more than 20%of total AUM, and the proportion of AUM in the five largest states in terms of AUM concentration further decreased from 94.6% as of March 31, 2016, to 66.1% as of June 30, 2022

Potent underwriting process, and risk management policies: As of Q1FY23, FY22, FY21 and FY20 gross NPA ratio was 3.6%, 5.7%, 5.5% and 1.1%, respectively, and net NPA ratio was 1.3%, 1.6%, 2.2% and 0.3%, respectively. According to Crisil, the company had the sixth lowest gross NPA ratio among the top 10 NBFC-MFIs in India during FY22, and average asset quality of 2.4% between FY15 and FY22 was the lowest among all NBFCMFIs operating in North India.

Risks

Higher NPAs: Even if credit monitoring and risk management policies and procedures are adequate and appropriately implemented, the company may not be able to anticipate future economic or financial developments or downturns, which could lead to an increase in NPAs. If NPAs increase or the credit quality of borrowers deteriorates, it could have an adverse effect on business, financial condition, results of operations and cash flows.

Competition from other MFIs, banks, and financial institutions: The company faces the most significant organised competition from other MFIs, banks and state-sponsored social programs in India. Traditional commercial banks as well as regional and cooperative banks may continue to increase their participation in microfinance.

Live Subscription

About the CompanyTata Technologies Limited, established in 1994 and headquartered in Pune, India, is a key player in IT consultancy and engineering design...

Introduction to Social Stock Exchange

A social stock exchange (SSE) is a platform or marketplace where socially and environmentally conscious organizations and impact-driven investors can...

Introduction to Corporate Governance

Corporate Governance refers to the set of processes, principles, and values governing how a company is managed and controlled. It is...

Twitter, the widely used microblogging platform, has faced difficulties in generating profits in recent years. In a bold move, Elon Musk acquired Twitter for...